The Ugly Middle

China's rare earth advantage was never geology. It was a system willing to absorb the residue, the discharge and the chemistry. Lynas shows how hard that is to copy.

The rare earths problem is almost always told as a China story. Beijing dominates separation, refining and magnet-making, so the answer is to build the same capacity somewhere else: more mines, more refineries, more separation lines, more magnets. That is true as far as it goes, and it does not go far enough. The harder lesson is that an ex-China supply chain does not stall only for want of ambition or capital. It stalls because the middle of the chain—the part between the mine and the magnet—is chemically nasty, water-hungry, residue-heavy and politically exposed in ways a balance sheet does not capture.

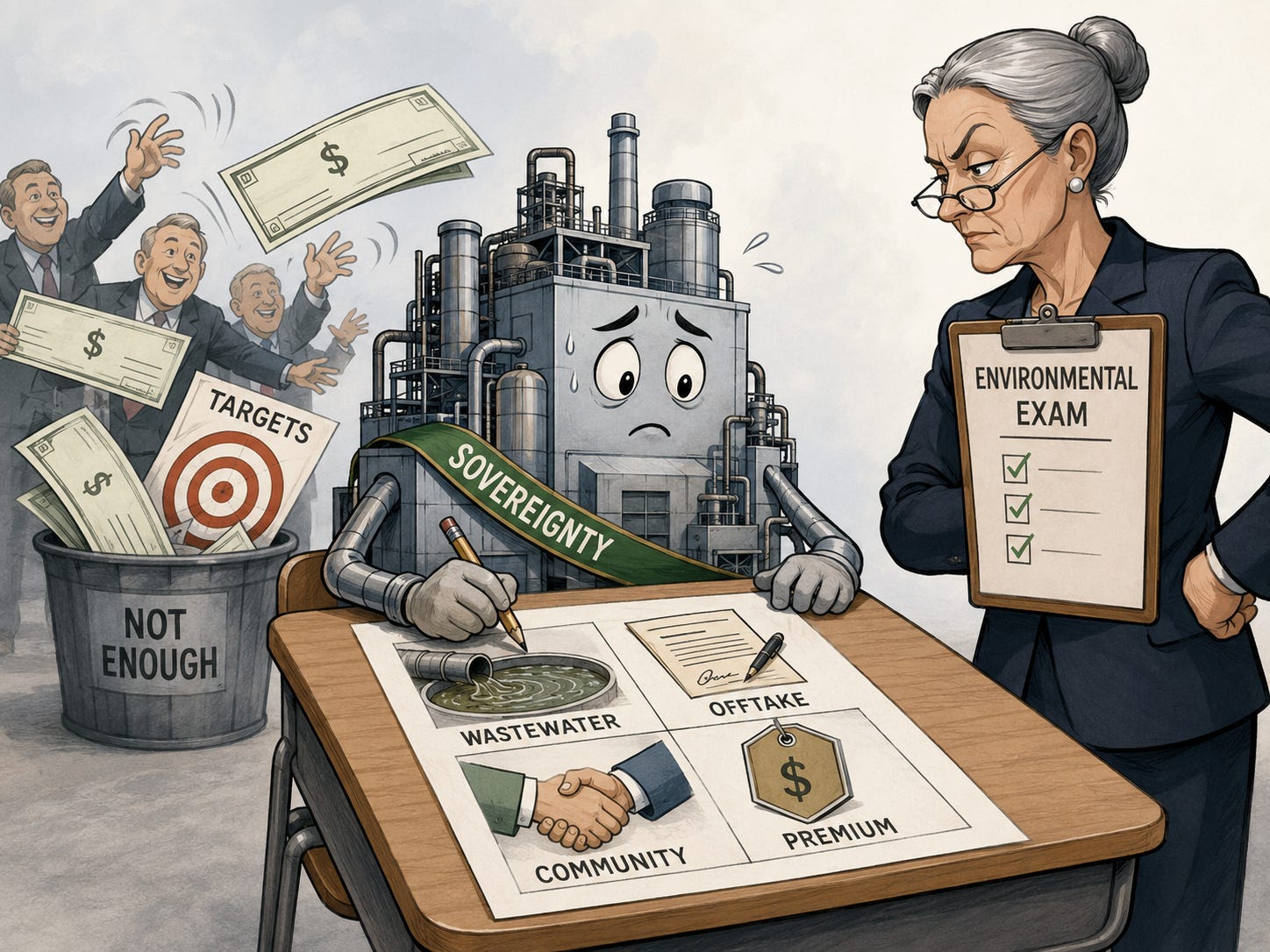

Lynas is now demonstrating exactly that, in two places at once. In June, Malaysia’s Department of Environment rejected the environmental impact assessment (EIA) for the proposed expansion of the Lynas Advanced Materials Plant (LAMP) at Gebeng, in Pahang—the most important rare earth separation facility outside China. The rejection was posted to the department’s website without a stated reason, but the opposition behind it is not mysterious. Gebeng’s cracking-and-leaching process generates Water Leach Purification residue: a low-level radioactive by-product that carries naturally occurring thorium, and that Lynas has spent more than a decade failing to find a permanent home for. The expansion would have meant more throughput and more residue, and the permit asked Malaysia to accept both.

This is easy to file as a local zoning fight. It is not. Lynas describes itself as the only commercial producer of separated light and heavy rare earth oxides outside China, supplying customers across Asia, Europe and the United States; Gebeng is where the cracking, the solvent extraction and the finishing actually happen, producing NdPr oxide alongside the heavy oxides—dysprosium, terbium, samarium—that defence and clean-energy supply chains are most anxious about. Targets, stockpiles, buyers’ clubs and alliance communiqués can all be announced from a podium. The material still has to be processed somewhere physical, and wherever that is, someone living nearby has to accept the residue, the discharge, the storage and the long environmental tail. That is the point at which strategy stops being a declaration and becomes a site plan.

Texas tells the same story from the opposite direction. Lynas’s proposed heavy rare earths plant at Seadrift was meant to be America’s near-term answer to its heavy processing gap, backed since 2023 by a Department of Defense commitment of up to roughly US$258 million. It has not moved cleanly from policy to plant. The design leaned on neighbouring Dow infrastructure to handle the acidic process wastewater, and that permitting pathway ran into trouble during 2025—exactly the unglamorous chemistry that rarely makes the strategy memos. Lynas told the market in its August results that there was “significant uncertainty” over whether the facility would proceed, and in what form; by late 2025 management was describing it as unlikely under prevailing terms. Seadrift is not formally dead. But it has been strategically downgraded—moved from “the plant that solves the problem” to “an option wrapped in wastewater, cost and offtake risk.”

What replaced it is the most revealing part. In March 2026, Lynas and the U.S. government restructured their arrangement away from funding the plant and toward buying the oxide: a binding letter of intent for a roughly US$96 million, four-year purchase of light and heavy rare earth oxides, with a guaranteed floor price of US$110 per kilogram for NdPr. The same US$110 floor has since been extended to MP Materials and, through Japan Australia Rare Earths, to Japanese buyers. Read that sequence carefully. When the build-out faltered, Washington did not walk away—it stepped in on the demand side, guaranteeing price and volume from assets that already exist. A government setting a floor price is an admission that the open market, left alone, will not finance the midstream. The economics of separation are too capital-heavy, too cyclical and too exposed to Chinese price power to clear on their own.

Now connect the two sites, because they are not parallel stories. When Seadrift stalled, Lynas’s heavy rare earth expansion shifted toward Malaysia. The capacity the United States wanted in Texas was, in effect, redirected to Gebeng—which is precisely where the permit wall then went up. The bottleneck did not disappear when it crossed an ocean. It moved. That is the structural fact: the constraint on ex-China processing is not where you put the money, it is where you can win permission to host the chemistry.

This is why China’s lead has never been about geology, and not really about subsidies either. China built a complete industrial system that was willing to absorb the ugly middle—the acid, the thorium, the discharge, the residue ponds—and to coordinate it across mining, separation, metals, alloys and magnets with guaranteed downstream demand pulling the whole thing forward. The magnet stage makes this starkest: China still accounts for the overwhelming majority of sintered NdFeB production, which means even a secure ex-China oxide supply does not, by itself, close the gap that matters most. Replicating that system means replicating not just the reactors but the social and environmental tolerance, the permitting throughput and the industrial coordination that made it run. Those are far harder to buy than a separation train.

There is also a distributional problem that will not stay quiet. Allied governments want secure dysprosium and terbium; automakers and turbine builders want reliable NdPr; defence planners want supply they can model. But the residue, the wastewater and the radioactive storage sit with whoever hosts the plant—Gebeng, Seadrift, Kalgoorlie. The asymmetry is becoming explicit in Malaysia, where the Gebeng expansion is now entangled with the fact that Lynas is supplying the U.S. defence base from Malaysian soil, a linkage that has drawn formal objections and sharpened local opposition well beyond the usual environmental complaint. When the strategic benefit is pooled across an alliance and the local burden is concentrated in one town, the politics do not remain technocratic for long.

So the lesson runs deeper than “permitting is hard.” Processing is where sovereignty has to sit its environmental exam, and passing it requires more than cheques and targets. It requires underwriting environmental performance rather than assuming it; securing demand and offtake directly, as the price floors now concede; sharing risk and benefit with host communities instead of exporting the residue to them; and paying the real premium that compliant, transparent, ex-China material costs—because it costs more than dependence on China ever did, and pretending otherwise is how these projects die.

Image credit: ChatGPT (OpenAI).

Lynas is neither villain nor victim here. It is the cleanest case study of the system everyone says they want: the mine, the technical depth, the customer base, the allied relevance, the strategic weight—all present, all real. And even here, with all of it in hand, the binding constraint is not ore. It is permission. The G7 can set its 2030 targets, Washington can write its cheques, Australia can market itself as a critical minerals superpower. But until the midstream can be permitted, financed, expanded and socially legitimised, the same wall will keep reappearing in different countries. Rare earth independence will not be delivered by ambition. It will be built, or blocked, in the wastewater permit.